Andrew Pannu posted on LinkedIn:

“The ADC space is blowing up:

• More than $125B in partnerships and M&A since 2019, including Pfizer’s $43B acquisition of SeaGen and a record $5.5B upfront deal (Merck / Daiichi) this year

• Hundreds of assets across thousands of trials

• 8 approvals in the last 5 years (13 total)

I pulled together 42 representative companies and charted the clinical assets of each, segmented by target and payload.

Exhibit 1: ADC Competitive Landscape

Some takeaways:

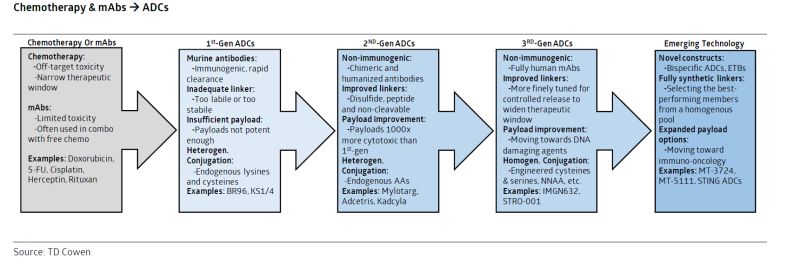

An ADC is essentially 3 modular components: an antibody, a payload (typically chemo) and a linker that connects the two. The idea is to combine the selective targeting of mAbs with the toxic lethality of chemo, such that only the tumor is impacted, rather than healthy cells.

Many approved mAbs are used in combination with chemo anyways, which negates the benefit of selective targeting. By minimizing off-target impact, ADCs can maximize the therapeutic window (increased efficacy at a lower dose, translating to a better side effect profile).

Exhibit 2: Evolution Towards ADCs (source: Cowen)

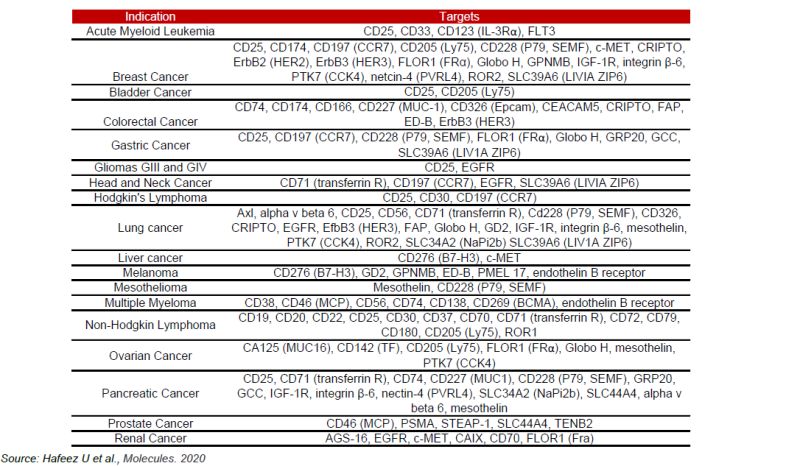

Key to the approach is selecting the right target. Ideally, the tumor should have a high level of antigen expression and healthy cells should have none. In reality, tumors are too heterogeneous, so companies settle for validated targets that are known to be more prevalent in tumors. Some ADCs exhibit a ‘bystander effect’ whereby the payload diffuses into adjacent cells that may not express the target antigen – an advantageous design in heterogeneous tumors.

Exhibit 3: ADC Target Antigens by Indication (source: Capital One)

The first ADC approved was Mylotarg in 2000 (later pulled from the market in 2010 and relaunched in 2017), although meaningful traction really started with later 2nd gen ADCs (such as Kadcyla and Adcetris) as the tech of each component improved. Since then, clinical and commercial wins have continued to rack up, including via ADC / IO combos (i.e. Padcev / Keytruda in bladder cancer at ESMO 2023).

Some recent financial stats:

• More than $7B in sales in 2022 (~33% YoY growth)

• Aggregate sales expected to exceed ~$20B by 2026 ($6B via Enhertu)

• More than $125B in partnerships, licensing and M&A deals since 2019

A lot of the differentiation between ADC players comes down to manufacturing prowess. Development is a multi-step technical process with a complex supply chain (components produced in separate locations). We’re seeing this theme with other emerging modalities as well.

Looking ahead, there’s potential for ADCs to move beyond oncology (i.e. Adcetris in sclerosis), as well as novel structural add-ons (bispecifics, RACs, PDCs, SMDC, DACs, etc.). Technological improvements will be key to watch – each successive generation has improved on efficacy / safety, and with the massive $ investment from several pharma companies, we can expect this to only increase. It’s likely that new brands, rather than biosimilars, are what cannibalize current ADC drug sales.”

Source: Andrew Pannu/LinkedIn

Cancer doesn’t take a day off – neither do we. OncoDaily.com – your go-to destination for the latest news, insights, and patient stories from the world of oncology!

{kind=link}

{kind=link}