Daniel Neumeier: Biopharma acquisitions H1/24

Daniel Neumeier, Life Sciences Specialist at L.E.K. Consulting, shared on LinkedIn:

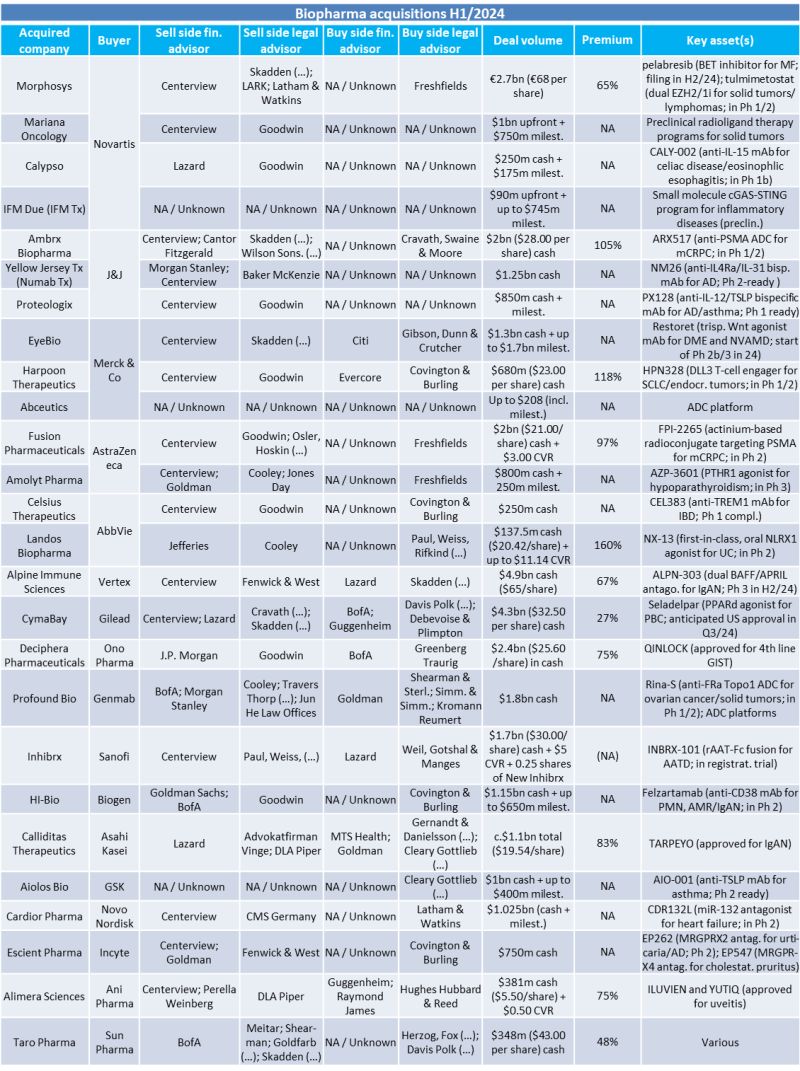

“Biopharma acquisitions H1/24

Number of deals and cumulative deal volume: 26 deals*, at least $34bn

Top 5 deals by volume:

· Alpine Immune Sciences – Vertex: $4.9bn (ALPN-303: pot. best-in-class dual BAFF/APRIL antagonist for IgAN; Ph 3 in H2/24)

· CymaBay – Gilead: $4.3bn (seladelpar: pot. best-in-disease PPARd agonist for PBC; anticipated FDA approval in Q3/24)

· Morphosys – Novartis: €2.7bn (pelabresib: BET inhibitor for MF; reg. filing in H2/24; tulmimetostat: dual inhibitor of EZH2/1 for solid tumors/lymphomas; in Ph 1/2)

· Deciphera Pharmaceuticals – Ono Pharmaceutical: $2.4bn (QINLOCK; widely approved for 4L GIST)

· Fusion Pharmaceuticals – AstraZeneca: $2bn + $3 CVR (FPI-2265: actinium-based radioconjugate targeting PSMA for mCRPC; in Ph 2)

Therapeutic focus areas of most active buyers:

· Novartis (4 deals): oncology (MF, solid tumors), autoimmune/inflammatory diseases (celiac disease, eosinophilic esophagitis)

· J&J (3 deals): inflammatory diseases (atopic dermatitis, asthma), oncology (ADC for mCRPC)

· Merck (3 deals): oncology (SCLC, neuroendocrine tumors, ADC platform), ophthalmology (DME, NVAMD)

· AstraZeneca (2 deals): oncology (mCRPC), endocrine disease (hypoparathyroidism)

· AbbVie (2 deals): autoimmune/inflammatory diseases (IBD, UC)

Premiums

· Highest: c.160% (Landos Biopharma – AbbVie; first-in-class Ph2 asset for UC)

· Average: 84% (excludes Inhibrix deal)

· Companies commanding above average premiums had assets that were (i) in Ph 1/2 or Ph 2, (ii) targeting oncology (ADC, radioconjugate, hard to treat tumors) or autoimmune/inflammatory indication

Advisors

Most frequent sell side financial advisors by # of deals (aggregate count based on lead / co-advisor status):

· Centerview Partners: 16 deals / c.62% of total deal count

· Lazard / Goldman Sachs / BofA: 3 deals / c.12% each

· Morgan Stanley: 2 deals / c.8%

Most frequent sell side legal advisors by # of deals:

· Goodwin Procter: 8 deals / c.31%

· Skadden, Arps, Slate, Meagher & Flom: 4 deals / c.15%

· Cooley: 3 deals / c.12%

· Fenwick & West / DLA Piper: 2 deals /c.8% each

Most frequent buy side financial advisors by # of deals (limited data):

· Lazard / Goldman Sachs / BofA: 2 deals / c.8% each

Most frequent buy side legal advisors by # of deals:

· Covington & Burling: 4 deals / c.15%

· Freshfields Bruckhaus Deringer: 3 deals / c.12%

· Davis Polk & Wardwell / Cleary Gottlieb Stehen & Hamilton: 2 deals / c.8% each

Acquired companies, by geographic origin

· 17xU.S. (65%), 7xEurope (27%; 2xDE; 1xCH, NL, UK, FR, SE each), 1xCA, 1xIL

Acquired U.S. companies, by area

· Bay area (5)

· Boston (4)

· San Diego (3)

· U.S. other (3)

· Seattle (2)

* deal volume >$100m and/or big biotech/pharma involvement”

Source: Daniel Neumeier/LinkedIn

{kind=link}